Over $1.6 billion in liquidity on major decentralized exchanges remained largely inactive during the first half of 2026, sidelining a vast amount of capital that failed to generate trading fees or contribute to market depth. This phenomenon highlights a key inefficiency within DeFi’s liquidity provisioning model that could have broad implications for traders and liquidity providers.

Idle Liquidity and Its Market Impact

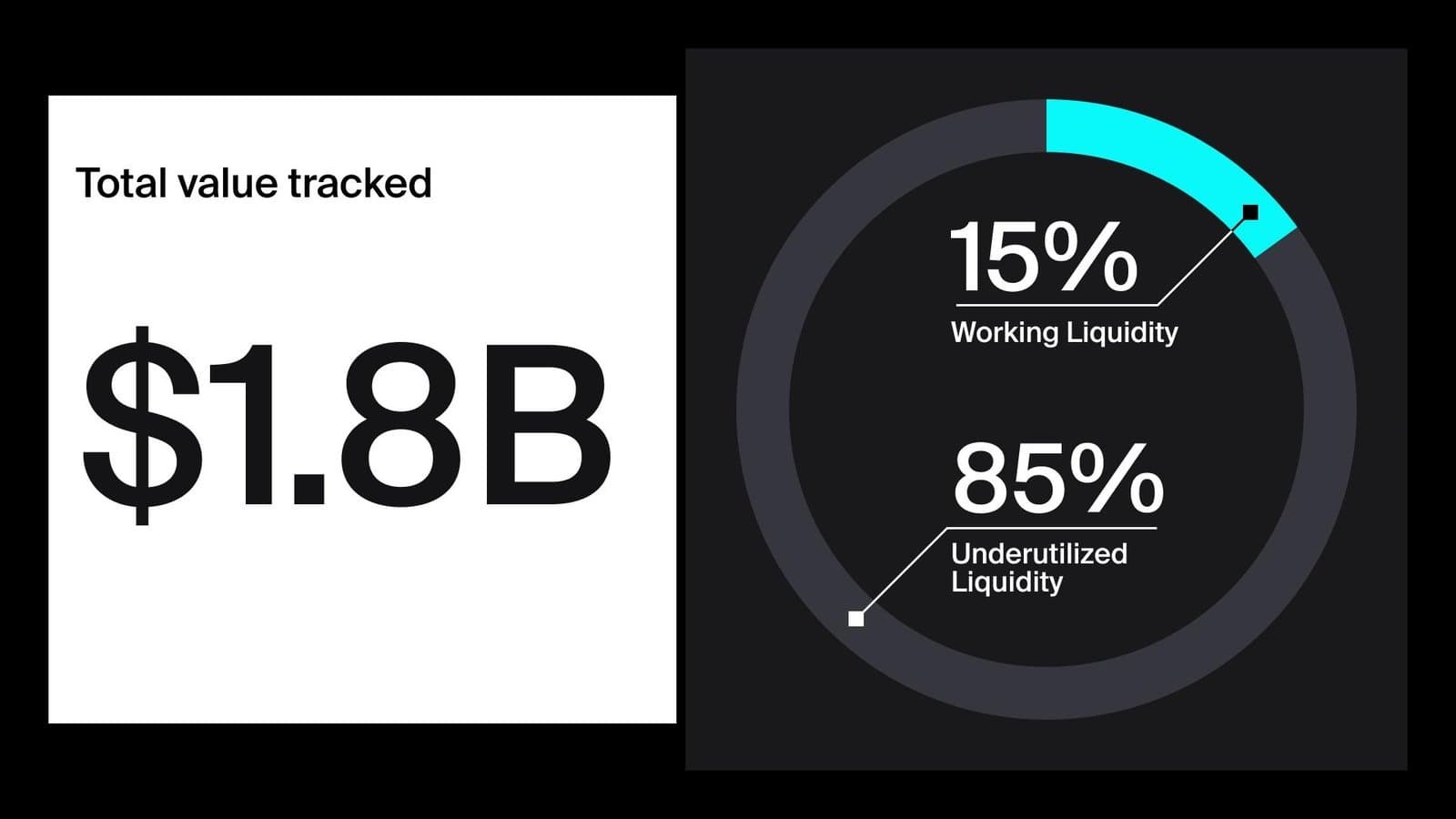

The research, conducted by Dune and commissioned by 1inch, tracked liquidity across Uniswap v3 and v4, PancakeSwap v3, and Aerodrome Slipstream across seven blockchains. It found that approximately 85% of the $1.84 billion in concentrated liquidity pools was underutilized, with nearly $542 million about 29.5% sitting fully outside active trading ranges in an average week. Capital in these out-of-range positions earns no fees since it is not engaged in active trades, effectively wasting liquidity that could otherwise bolster market efficiency and fee generation.

Concentrated liquidity pools operate by allowing providers to specify price ranges where their funds are deployed. When prices move outside these pre-set ranges, the liquidity effectively becomes dormant until adjusted or the price returns. For instance, an ETH/USDC pool position set between $2,000 and $2,500 stops generating fees if ETH’s price moves beyond this band. Providers face a trade-off: stay exposed to price adjustment risks and transaction costs to maintain active positions, or accept periods of zero earnings.

Why This Matters Going Forward

The presence of so much idle liquidity undermines one of DeFi’s key value propositions: efficient, continuous market making without centralized intermediaries. As traditional financial firms push deeper into tokenized funds and blockchain settlement, and retail platforms onboard more users, the cost of stranded capital could amplify. Markets may experience thinner effective liquidity and lower fee generation as more capital remains out of play.

According to Filippo Armani, research lead at Dune, decentralized exchanges have become one of the deepest crypto markets, yet much of the liquidity is “not yet fully at work.” If this dynamic persists, liquidity providers may see diminishing returns relative to the funds they allocate, possibly discouraging participation or pushing them toward more flexible strategies.

This liquidity inertia challenges assumptions about DeFi’s maturity and raises questions about how concentrated liquidity models might evolve. Adjustments may be needed to incentivize providers to manage ranges dynamically or to develop mechanisms that utilize out-of-range capital more effectively.

This material is informational and not financial advice.